日本経済新聞 2008/10/15

石化製品の輸出価格下落

アジア市場 ナフサ安や中国需要減

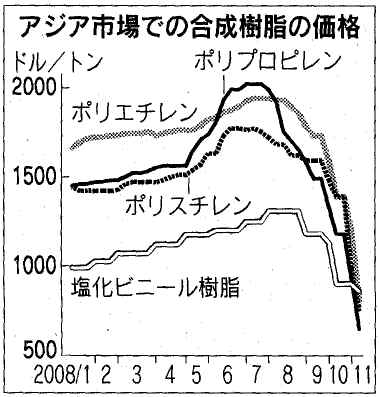

合成樹脂など石油化学製品のアジアヘの輸出価格下落が続いている。最近の原油安を受けて基礎原料のナフサ(粗製ガソリン)が下落し、製品価格の下げを招いている。最大の輸出先である中国の需要が落ち込んだ影響も大きい。中国から最終製品を購入する米国などの景気低迷も深刻で、当面は輸出価格の反転は見込めない。

包装用フィルムなどに使うポリプロピレン樹脂の東アジア地区の価格は1トン1330ドル(中心値)とピーク時の7月に比べ35%安い。塩化ビニール樹脂は8月の高値から14%安い1130ドル(同)。ほかの樹脂も含め、なお先安観が強い。

下げの最大の要因はナフサ安。アジア市場のスポット価格は7月に1トン1248ドルと過去最高値を付けた後、下げ基調に転じた。14日は584ドル(12月前半入着分)まで落ち込んだ。

もう一つの要因が中国の需要縮小だ。中国ではここ数年、個人消費の伸びに加え、北京五輪向け投資による石化製品の需要が拡大してきた。道路のアスファルトの下に敷くポリスチレンシートなどインフラ需要が盛り上がったが、五輪開催前にピタリと止まった。

米景気減速が追い打ちをかけた。9月から家電製品の包装材や自動車部品向け樹脂などの調達意欲が「目に見えて減った」(商社のエチレン輸出担当者)。9-10月は米国のクリスマス商戦に向けた素材の需要期にあたるが、玩具に使う塩ビ樹脂などの調達意欲も弱い。

中国には「石化製品の転売で利ザヤを稼ぐトレーダーが存在する」(大手化学メーカー)。先安観が強い現在はこうした需要もない。下落傾向は当面続きそうだ。

石化製品 10ヶ月連続輸出減 中国の設備ラッシュも背景

石油化学製品の輸出量も長期にわたり減少傾向が続いている。中国の旺盛な需要に支えられ増勢をたどっていた輸出は8月、基礎製品のエチレン換算で155千トンと前年同月比9%減。昨年11月を境に減少に転じ、10カ月連続で前年同月実績を下回った。

国・地域別の輸出先(2007年、輸出額べース)は香港を含む中国が50%を占める。韓国(16%)、台湾(13%)がこれに続く。

「価格が下がっても注文が入らず、モノが動かない」。石化製品の中間原料を扱う商社の担当者が漏らした言葉は最近の輸出市場の実態を的確に表している。

日本のメーカーは食品容器に使うポリスチレン原料のスチレンモノマーなどを減産し、輸出余力が乏しくなった。中国国内で石化プラントが相次いで稼働したことも日本からの輸出減につながった。

日本メーカーが原料高騰時に生産した製品の安値での輸出を手控え始めたことも一因だ。世界経済の動揺は続いており、石化製品の輸出市場にも明るさは見えない。

NY原油 マネー流出鮮明 06年7月以来建玉少なく ファンド手じまい売り

ニューヨーク原油先物市場からのマネー流出に拍車がかかっている。米商品先物取引委員会(CFTC)によると、市場の資金量を示すWTI(ウェスト・テキサス・インターミディェート)原油の建玉総数は7日時点で108万7600枚(1枚=千バレル)。前週比4800枚減った。

3週連続で減少し2006年7月以来の低水準に落ち込んだ。3月中旬には直近で最高の149万8千枚に達した。その後、6月までは120万ー140万枚を維持したが、7月から相場の下落とともに減っている。

欧米金融市場の混乱でヘッジファンドなど機関投資家が買い持ちを整理するため手じまい売りを急いだことが主因。新規の買いが入りにくく、決済分だけ建玉が減った。

SCM証券の佐野慶一社長は「投資家は金融不安からリスク資産を削減しており、一段の下げもありうる。当面は荒い値動きが続く」と分析する。

2008/10/15 Platts

US PVC export values hit 22 month low, down $300/mt over 4 weeks

PVC export values

continued to slide this week to be talked at sub-$800/mt levels

on an FAS basis, sources said. Participants reported a workable

export number out of the US Gulf would have to be near $740-750/mt

FAS Houston.

Still there remained a gulf between buyers and sellers as

producers were not yet ready to offer at such low levels.

"Producers are not willing to subsidize that much

money," said a source.

One supplier suggested that if he were to offer, the number would

be closer to $800-810/mt FAS Houston. The assessment Wednesday

was at a 22-month low and down $300/mt over the course of four

weeks, closing at $765-$775/mt FAS Houston. According to Platts

data, PVC exports were assessed at $770/mt FAS Houston back on

December 20, 2006.

Participants pointed to anemic demand and plummeting feedstocks

as key drivers behind the downward movement.

Meanwhile spot activity was thin as the rapid movement in pricing

coupled with the disconnect between buyers and sellers made deals

hard to come by.

"By the time you can fix a deal, the price changes and the

buyer backs out," said one source.

Another trader confirmed adding, "It takes three times as

much work as it used to in order to get a deal done."

2008/10/16 Platts

Taiwan Vinyl Chloride

Monomer to keep VCM plant shut till end Oct

Taiwan Vinyl Chloride Monomer has decided to keep its 340,000

mt/year VCM plant at Kaohsiung shut for the rest of October as

buying appetite from its key Chinese customers appeared set to

remain weak for the rest of the fourth quarter, a company source

said Thursday morning.

The company had shut its plant on September 1, initially for 15

days on weak demand, mainly from China. The company has since

extended the shutdown twice. As a result of its extended

shutdown, the company had not been purchasing spot ethylene

dichloride feedstock for the last three months.

Spot VCM prices are likely to plummet the $650/mt CFR China mark,

given the drop in feedstock naphtha prices.

Prices of open spec naphtha cargoes on a CFR Japan basis

continued to plunge when markets opened in Asia Thursday, led by

falling Western crude benchmarks and sluggish petrochemicals

demand.

Naphtha cargoes for delivery in the first and second half of

December and first half of January were each down $33.75/mt to

$465.25/mt, $484.25/mt and $500.25/mt, respectively.

2008/10/16 Platts

SK Energy to shut No. 1

cracker from Nov on weak demand

South Korea's SK Energy

will shut its No. 1 naphtha-fed steam cracker in Ulsan

end-October or in November due to weak petrochemical demand, a

company source said Thursday.

"We are shutting the cracker from the end of October or from

November as downstream demand is so poor," the source said.

The No. 1 cracker has been running at 75% capacity since April

due to weak demand for petrochemicals.

SK Energy has not decided on the length of the shutdown, but the

source said it would last at least until the end of the year.

Several naphtha cracker operators have reduced operating rates to

cope with high inventory amid weak demand, but SK Energy's No. 1

steam cracker will be the first to shut completely, industry

sources said.

However, market sources said it would have only a limited impact

on the Asian ethylene market, which has been in a downward trend

since early July.

"The production capacity of the No. 1 cracker is very small.

The shutdown's impact will be limited," a trader said.

The No. 1 steam cracker can produce 200,000 mt/year of

ethylene and

140,000 mt/year of propylene. The average ethylene production

capacity of Northeast Asian cracker operators is 415,000-627,000

mt/year.

"The Asian ethylene market has not been supported even by

two large cracker shutdowns in Taiwan," the source noted.

In Taiwan, Formosa Petrochemical shut its No. 2 naphtha-fed steam

cracker at Mailiao October 9 due to a compressor problem. The

unit, which is able to produce 1.03 million mt/year of ethylene

and 515,000 mt/year of propylene, will be shut for two weeks.

Formosa's No. 3 naphtha-fed steam cracker at Mailiao remains shut

until October 19 after being idled September 3 for turnaround. It

is able to produce 1.2 million mt/year of ethylene and 600,000

mt/year of propylene.

Northeast Asian ethylene prices were pegged at $795/mt CFR early

Thursday, less than half the record high of $1,695/mt CFR

Northeast Asia reached July 10.

Meanwhile, SK will maintain operating rates at its No. 2

naphtha-fed steam cracker in Ulsan at 100% capacity. It is able

to produce 670,000 mt/year of ethylene and 360,000 mt/year of

propylene.

日本経済新聞 2008/10/18

ポリスチレンが初の20万トン割れ 四半期軍出荷7-9月 素材に景気減速の影

日本スチレン工業会が17日発表した汎用樹脂ポリスチレンの7-9月期の国内出荷は、前年同期比4%減の約198千トンだった。統計を取り始めた1990年以来、四半期での20万トン割れは初めて。

9月単月も前年同月比4%減の約61千トンと過去2番目に低い水準で、景気減速の影響が素材分野でも深刻化してきた。

ポリスチレンは自動車部品になるポリプロピレンなどと並ぶ五大汎用樹脂の一つ。食品容器や事務機器のボディー、液晶パネル部材といった幅広い用途に使われる。

7-9月期の用途別では前年同期並みだった包装用以外はすべて前年同期の実績を下回った。

減少幅は事務機器や液晶テレビなど電機工業用が9%、玩具などの雑貨産業用は7%、住宅向け断熱材などになる発泡用が3%だった。

2008年10月22日 Chemnet Tokyo

SPDC、PEの輸出価格を再度大幅に引き下げ

中国・東南アジア向けの提示価格1,100ドルに

サウディ石油化学(SPDC)はこのほど、中国並びに東南アジア各国の大手フィルムメーカーとディストリビュータ各社に対して日・サ合弁企業「シャルク」

の直鎖状低密度ポリエチレン(商品名;QAMAR)の11月の輸出価格をCFRトン当たり1,100~1,110ドルとしたい考えを伝えた。ナチュラル品

種を同1,100ドル、高透明品種を同1,110ドルとしたい意向。中国向けも東南アジア向けも同じ価格とする。

同社による10月の納入価格は同1,480~1,490ドルであった。9月の価格を250ドル下回る低レベルでの契約となったが、11月分はそれをさら

に380ドルも下回ることになる。1ヵ月でこれだけの幅の値下げは初めて。今年の最高値の7~8月の価格に対しては720ドル安となる。しかも、関係筋の

多くは中国や東南アジア各国の需要家がこれをすんなり受け入れるかとなると大いに疑問と見ている。

同社が11月分についても大幅な引き下げを実施することにしたのは、アジア地域全域の需要家からの引き合いが減少の一途をたどっているためスポットものの相場が1週間ごとに同100ドル前後下がって先週末の時点で同1,100ドルまで下降したことによる。

最大の消費国である中国の需要家は、ショッピングバッグの輸出の減少と内需の不振、さらには原油ならびにナフサの国際相場の急落等を睨んで同樹脂の買い控えを強化しているところ。このため、原油とナフサ価格が反騰しない限り発注量が回復することにはならないと見られている。

過去の報道

7月 1,830~1,840ドル

8月 1,830~1,840ドル

9月 1,730~1,740ドル

10月 1,530~1,540ドル

11月 1,100~1,110ドル

2008/10/20 Platts

China's supermarket

plastic bag use could halve in 2009

Demand for plastic

bags in China's supermarkets could slump 40-50% next year due

to a ban on free plastic bags, a Sinopec source said during a

conference organized by the Dalian Commodity Exchange

Tuesday.

China's General Office of the State Council imposed

restrictions on the use of plastic bags from June 1 as part

of its campaign to protect the environment and conserve

energy. The office ordered a ban on the production, sale and

use of ultra-thin bags with a thickness of less than 0.025

mm.

At the same time, supermarkets and shops were banned from

distributing free plastic bags. Retailers were instructed to

clearly label plastic bag costs and charge these separately

to consumers.

According to Sinopec, plastic bag producers number between

130,000 to 150,000 in China, of which around 2,000 focus on

producing hand-carry plastic bags commonly used in retail

outlets.

These producers use polymers like high density polyethylene,

linear low density polyethylene, low density polyethylene and

polyvinyl chloride as materials.

Supermarkets in China consumed 400,000-500,000 mt of plastic

bags in 2006, accounting for around 30% of domestic plastic

bag demand.

"China's plastic bag ban has significantly impacted

supermarkets and stores, noticeably curbing demand for

plastic bags. Retail use of plastic bags could plunge 40-50%

next year," Sinopec Economics and Development Research

Institute's Gao Chun Yu said during the conference.

| 2008年10月22日

Chemnet Tokyo |

| |

| アジアのエチレン相場、ついに700ドル割れ |

| 一気に05年春のレベルまで戻る |

大手商社各社によると、アジア地域におけるエチレンのスポットもののCFR価格がついにトン700ドルを割り込んだ。

直近の価格は、極東でも東南アジア諸国でも同680ドル前後となっている。10月第2週の平均に比べて130ドル前年下がったことになる。最近の最高値

の昨年11月に比べると1,000ドル安となる。同700ドル割れは、05年6月の平均の670ドルいらいとなる。原油とナフサのスポット相場の続落を睨

んでの誘導品各社と地域トレーダの買い控えによるもの。実際の取り引き数量は縮小の一途をたどっている模様。シンガポールを除くアジア各地でエチレンと誘

導品の減産が一段と進んでいる。 |

| 2008年10月27日 |

| 三井化学ポリウレタンがTDIの大幅減産へ |

| 中国の需要の激減に対応、今週末から50%操業に |

三井化学ポリウレタンは、中国の需要の激減に対処してTDIの生産を大幅に縮小することになった。今週末から、大分と鹿島の両工場の設備の稼働率をいずれも50%に引き下げる。今年末まで継続する考え。これだけの大幅減産に踏み切るのは初めてという。

同社が保有するTDI設備の年間生産能力は、大分工場12万トン、鹿島工場11万7,000トンの合計23万7,000トン。世界3大メーカーの一角を

占めている。両工場で生産するTDIの圧倒的多数を中国を中心とした海外への輸出でさばいてきた。9月までは、国際需給バランスが均衡していたため安定し

た輸出を継続でき、また価格もCFRベースでトン4,000ドル台という比較的高値を維持できた。

しかし、いわゆる“リーマンショック”が表面化してからは中国からの引き合いと注文が激減。10月の契約数量が大幅に縮小するとともに価格も一気に

3,000台に急落する事態となった。そこで同社では10月入りとともに稼動率を80%に落として模様を眺めていたが、その後も一向に中国の需要が回復の

兆しを見せないためついに50%という未曾有の減産に踏み切ることにしたもの。

中国の需要が急激に縮小してきた要因について同社では、寝具や家具、マットレスといったウレタン使用製品の対米輸出がばったり止まったことと、中国の需

要家の間にTDIの輸入価格値下がりが必至と予想する向きが急速に増えて買い控え機運が一気に広がってきたことを挙げている。

後者はともかくとして、前者については急速な事態の改善は期待できないというのが同社をはじめとした関係者に共通した見方となっており、このため同社で

は年内いっぱいは5割操業を継続していくほかないと判断している。大手商社の中には、同社等の減産が続けば遠からず中国の市中在庫が不足することになるの

で年明けには引き合いがあるていど活発になると見る向きが多い。

|

2008/10/29 Platts

US export PVC prices hit

5-year low with offers at $600/mt FAS

Export PVC prices in the

US continued to spiral lower this week hitting their lowest

levels in over five years. Following lower Asian values, US PVC

export prices plummeted further with offers heard at $600/mt FAS

Houston this week. A precise number was difficult to pin down,

sources said, as buyers were reluctant to do deals given rapidly

decreasing prices.

"It's hard to conclude business," said one source.

"There are few inquiries and buyers will then go shop around

and then come back with a price that's $50 lower."

Bids to domestic suppliers were heard earlier in the week at

$600/mt FAS Houston and were talked lower by mid-week.

"If you were to offer $600/mt right now, you could probably

get a deal done but then you wouldn't be able to sell," said

one participant. "You would be stuck with high-priced

material." Since the end of August, PVC export values have

fallen over $600/mt on the back of weak demand.

The last time prices were under $600/mt was back in September,

2003 when PVC export values were assessed at $590/mt FOB USG.

Sources expressed mixed sentiment on where the bottom might be

with some participants pointing out that producers will begin to

slash rates or shutter production. "I don't see how it can

go much lower," said one source.

Furthermore, credit issues continued to add problems to an

already complicated milieu as participants reported continued

difficulties in obtaining credit letters. "Banks are not

comfortable issuing letters of credit let alone extending

credit," said a source.

Sources anticipated that there was room for prices to fall

further with some estimating the floor to be as low as $500/mt

FAS Houston.

| 2008年11月12日 |

| 三井化学、PTAの対中輸出価格600ドルを目指す |

三井化学はこのほど、中国の大手ポリエステル企業各社ならびにトレーダー筋に対してPTA(高純度テレフタール酸)の11月の輸出価格をトン当たり

CFR600ドルとする考えを示して了承を求めた。最近のスポット品のCFR価格が同580~590ドルで推移している点を考慮して同600ドルを提示

し、受け入れを要請したもの。

同社は、過去数ヶ月の輸出分もほぼスポット相場と同じレベルの価格に設定してきた。スポットものの7月以降の月間平均価格は、7月が1,170ドル、8 月が1,050ドル、9月が860ドル、10月が720ドルと下降の一途をたどってきた。したがって、同社の輸出価格も同じ幅で下降を続けてきたことにな

る。

|

日本経済新聞 2008/11/20

合成樹脂、アジアで急落 ナフサ値下がり

中国の買い付け鈍化

食品包装材などに使う合成樹脂の価格がアジア市場で急落している。原油安を背景に基礎原料のナフサ(粗製ガソリン)が値下がりしており、夏場ごろの高値からの下げ率は最大で7割に達した。景気後退で中国の加工業者の樹脂の買い付け意欲は乏しく、取引量も急減している。アジア価格の急落は国内の取引価格には下げ圧力になる。

下げ幅が最も大きいのは、包装材料に使うポリプロピレン。足元の価格は1トン650ドル(中心値)で1カ月で半値に落ち込んだ。7月の高値からは68%急落した。食品フィルムに使うポリエチレンや、家電の外枠に使うポリスチレンもともに夏場のピークから6割近く安い。

水道管などに使う塩化ビニール樹脂は現在、1トン860ドルと高値からは34%の値下がりにとどまる。ただ、「一部で800ドル近い取引もある」(商社)との指摘もあり、価格基調は弱い。

大口の需要家である中国の加工業者が買い付けを控えている。世界景気の減速で欧米での最終製品の需要が盛り上がりを欠いているため、中国の加工業者は原料樹脂の在庫積み上げを見送っているようだ。ナフサのスポット価格が7月のピーク時から8割値下がりし、合成樹脂の先安観が強いことも影響している。

塩ビ工業・環境協会によると、塩ビ樹脂の10月の輸出量は約43,900トンで前年同月比41%減った。円高・ドル安で日本からの輸出環境が悪化している面があるものの「中国の塩ビ加工業者は買付に慎重だ」(大手塩ビメーカー)

アジア市場でのナフサや合成樹脂の値下がりは国内価格の下げ圧力になる。国内需要家はナフサ安をみて値下げ要求を強めている。